I am faced with the following dilemma: 1. I believe in rules and strategy-based trading. I believe one must not deviate from the “rules”. 2. I can “see” risks that are not incorporated into my model(s). Let me put this in context. From a quant point of view (at least a simple, price-based quant model) a …

strategy development

Raging Bull

It seems that most of the strategies that are in the public sphere, are consciously or unconsciously trying to prevent the large 2007-2009 draw-down. From simple to complex Tactical Allocation Systems, to mean-reverting strategies, to volatility based strategies, pairs strategies, etc. They all avoid (in hindsight) the biggest market crash that most of us have experienced. But what happens …

Backtesting Options: Selling SPY Puts on RSI(2)

Let’s try the good old strategy for RSI(2) mean reversion.Buy on Rsi(2)<30Sell on Rsi(2)>60Execution is on the Open of the next day.This is what trading the SPY etf looks like. How about using the same signals and selling 10, 1-point away from the floor price, front month Puts.* Again, we sell 10 Puts right below …

Mon AMMI

No, it’s not french and it’s not the movie.It’s a fast-N-rough “Adaptive Multi strategy Multi Instrument” model. Let’s assume we want to trade mean-reversion: If price moves down we buy, if it moves up we sell. Possible Indicators from the blog-o-sphere:RSI(2),RSI(3),RSI(4)DV2 here and hereBSI here or hereBoilingerBandsCRSI hereTD9 here Question 1: Which Indicator to use? One …

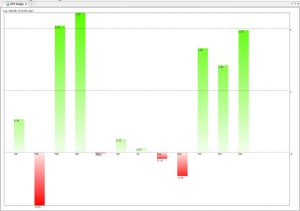

Seasonals – SP500, Euro

Here’s the strategy: Each month we buy at the Open of the first day of the month and sell at the close of the last day of the month. Here’s the average profit loss for the S&P500 Etfs, SPY (yahoo:SPY). Data from 1993. This chart shows that for example if we bought every December @ …