I am faced with the following dilemma:

1. I believe in rules and strategy-based trading. I believe one must not deviate from the “rules”.

2. I can “see” risks that are not incorporated into my model(s).

Let me put this in context.

From a quant point of view (at least a simple, price-based quant model) a jump in VIX of 30%+ does signify an event. Some strategies will enter a mean reverting mode, some will sell-off to avoid a volatile environment, some will jump in and double down, some will sell options, etc.

Quantitatively speaking, one may start by looking at other instances where the VIX jumped more than X% and see what happened in the next few days (here, here , here and here).

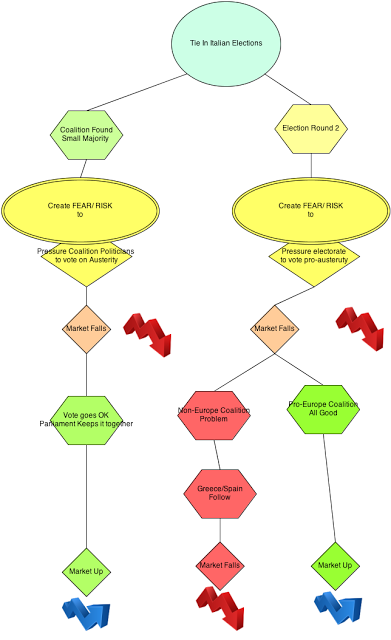

From a fundamental (and common sense) point of view, the event that caused the VIX to jump was the outcome of the Italian elections. This is by no means a minor event. It is the first time the south European public votes against German imposed austerity, something that surprisingly has not yet happened even in Greece (@34% unemployment… how long can that last?), Spain (@20%+ unemployment) or more recently, Cyprus. This could cause fundamental long term changes to Europe and affect the U.S. market as well.

For illustrative purposes only, I created a simplistic diagram of outcomes following the Italian Elections:

No-matter what the final outcome, halfway through the diagram, there is a lose-lose situation. In other words, one can argue that until the Italian Elections are conclusive, it is not in the interest of the ECB or Germany to stabilize the markets, especially the Italian sovereign spreads. So if we were to accept the logic of this diagram, even the market-positive outcome assumes a bearish transitory period.

So how does one incorporate this theoretical “belief” without diverging from the systems in place?

One solution is to do nothing and stick to your guns.

Another solution is to get out of the market and stay cash.

But when do you come back in? How do you decide when the danger is over. When the market has already advanced another 15% while sitting in cash?

A third solution is to turn-on alternative strategies. These could be tail-protection* strategies.

There are many ways to protect from tail risk. Some are better than others. Most cost money in a bullish environment. An obvious example is buying puts. That could protect your positions but if the crash never materializes, the cost of the puts would eat into the returns.

Well, nowadays a retail investor has access to other protection than just buying puts.

One way to find such a strategy is to split existing strategies into their short and their long components and trade just the short one as a hedge to existing positions.

Take MarketSci’s proposed strategy as an example. As of yesterday the VIX futures are barely in contago, which means that the strategy is ready to go long the VXX.

Here’s another strategy that it’s short side may work in a bearish environment.

Conclusion:

One way to solve the subjective opinion vs objective model dilemma is to create a strategy that is both agreeable to your subjective opinion and has done ok historically. Then instead of trading the subjective belief you trade the model that incorporates it.

If you cannot find a good model that incorporates it, chances are you shouldn’t trade those beliefs in the first place.

*Tail protection is a fancy way of saying protection from abnormal events such as sudden market crashes.

** This information is not to be construed as financial or investment advice. No information herein should be taken as a recommendation buy, hold or sell any investment or to use a specific investment strategy

Leave a Reply