Let’s try the good old strategy for RSI(2) mean reversion.Buy on Rsi(2)<30Sell on Rsi(2)>60Execution is on the Open of the next day.This is what trading the SPY etf looks like. How about using the same signals and selling 10, 1-point away from the floor price, front month Puts.* Again, we sell 10 Puts right below …

SPY

CBA – Quick test drive

Inspiration strategy: http://empiritrage.com/2013/01/21/correlation-based-allocation/ Quoted from Empiritrage.com:“We propose a model that is designed to identify bull-market and bear-market regimes. We examine correlation between stocks and bonds as a signal. Our hypothesis is that negative correlation between long bonds and stocks represents a bear-market regime, and a positive, or non-existent correlation, reflects a bull market regime.The model calculates …

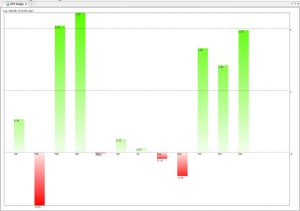

Seasonals – SP500, Euro

Here’s the strategy: Each month we buy at the Open of the first day of the month and sell at the close of the last day of the month. Here’s the average profit loss for the S&P500 Etfs, SPY (yahoo:SPY). Data from 1993. This chart shows that for example if we bought every December @ …

Connors RSI – Part 1

One of the readers of this blog, Mark, alerted me to a new indicator/system published from Connors/Alvarez : The ConnorsRSI. What is the ConnorsRSI? It consists of three components:a. Short term Relative Strength, i.e., RSI(3).b. Counting consecutive up and down days (streaks) and “normalizing” the data using RSI(streak,2). The result is a bounded, 0-100 indicator.c. Magnitude of the move …

Better than mean-reversion? An Adaptive Multi-Strategy System

Mean reversion strategies have been very popular since 2009. They have performed exceptionally well for the past 10 years, performing well even during the 2008-09 bear market. Different versions have been popularized, notably by Larry Connors and Cezar Alvarez (previous post) as well as many others in the blog-o-spere such as David Varadi of CSS analytics (DV2) and Michael Stokes @ MarketSci. …

Read moreBetter than mean-reversion? An Adaptive Multi-Strategy System