In the previous post I showed how one can implement “regime” switching to create a strategy that switches between a mean-reverting and a momentum sub-strategy. Can we do something similar (or better) using Fuzzy Logic? Here’s the setup: (here for some Fuzzy Logic backround) We create a basic membership function for the RSI(2) indicator: …

Archives for September 2013

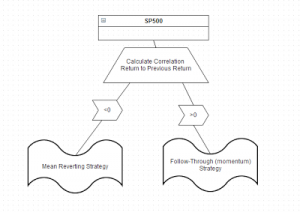

Simple Regime Switching for SP500

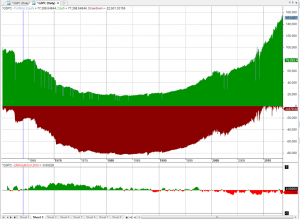

image from http://brucekrasting.com/ Let us consider two possible ways to trade the SP500. 1. If the index falls today, we buy tomorrow at the open. This is a “mean-reversion” strategy. 2. If the index rises today, we buy tomorrow at the open. A “follow-through” strategy. From the graphs below, we can see that neither of …